TL;DR

ChatGPT can now connect to your bank accounts via Plaid, giving OpenAI access to the most intimate data category left.

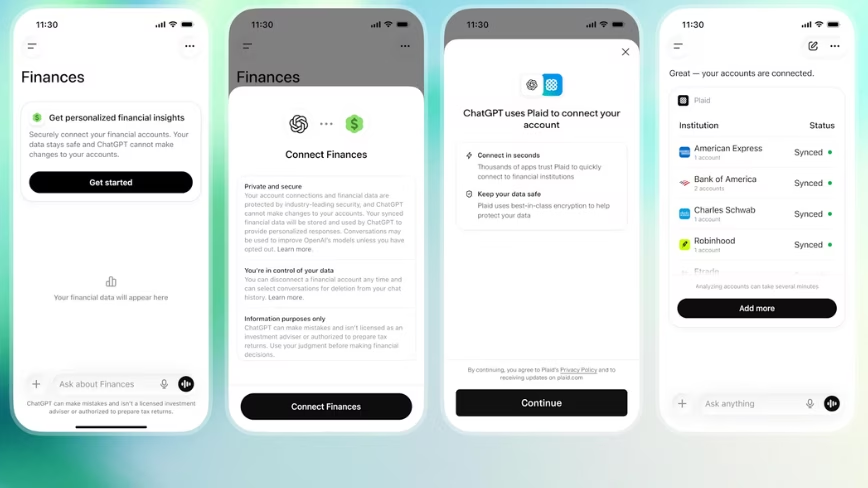

OpenAI has launched a personal finance experience inside ChatGPT, letting subscribers connect their bank accounts, credit cards, investment portfolios, and loan accounts to the chatbot and ask questions grounded in their actual financial data. The feature, released on 15 May, is available in preview to US-based ChatGPT Pro subscribers on web and iOS, with support for more than 12,000 financial institutions through a partnership with Plaid.

The integration is straightforward. Users open a new “Finances” tab in the ChatGPT sidebar or type “@Finances, connect my accounts” in any conversation. ChatGPT guides them through linking accounts via Plaid, the same connectivity layer used by Venmo, Robinhood, and most major budgeting apps. Once connected, the chatbot generates a dashboard showing portfolio performance, spending patterns, subscriptions, and upcoming payments. Users can then ask questions like “what did my last holiday actually cost me?” or “help me build a plan to buy a house in five years.”

OpenAI says ChatGPT can see balances, transactions, investments, and liabilities, but cannot see full account numbers or make changes to accounts. Users can disconnect services at any time through settings, and synced data is removed within 30 days. Financial memories, the contextual information ChatGPT stores about a user’s goals and priorities, can be viewed and deleted from the Finances page.

The company says more than 200 million users already ask ChatGPT finance-related questions every month. The new tool is designed to move those conversations from generic advice to answers grounded in a user’s actual money. The feature runs on GPT-5.5, OpenAI’s latest reasoning model, which the company says is stronger at the context-dependent reasoning that personal finance questions require. OpenAI worked with more than 50 finance professionals to build an internal benchmark, on which GPT-5.5 Thinking scored 79 out of 100 and GPT-5.5 Pro scored 82.5.

The launch comes exactly one month after OpenAI acquired Hiro Finance, an AI-powered personal finance startup founded by Ethan Bloch, who previously sold neobank Digit to Oportun for more than $200 million. Hiro was backed by Ribbit Capital, General Catalyst, and Restive. OpenAI described it as an acqui-hire: Hiro shut down on 20 April, deleted all user data by 13 May, and Bloch’s team of roughly ten people joined OpenAI. The company said the Hiro team’s expertise was useful in launching the finance feature but did not specify whether the entire product was built by them. Hiro was itself the second fintech acquisition for OpenAI, following its purchase of investment app Roi approximately six months earlier.

OpenAI is also working with Intuit on deeper integrations. Future capabilities could include understanding the tax implications of a stock sale, estimating credit card approval odds, or scheduling a session with a local tax professional, all inside ChatGPT. The Intuit partnership, if it materialises at the scale described, would move ChatGPT from a passive advisory tool to something closer to a financial services platform.

The competitive context is immediate. Perplexity launched its Computer for Professional Finance product on 5 May, aimed at analysts and investors, with 40-plus built-in finance tools pulling from SEC filings, FactSet, and other institutional data sources. On 14 May, Perplexity expanded its consumer finance capabilities by adding Plaid integration for personal brokerage, checking, savings, and credit card accounts, the same infrastructure OpenAI announced one day later. Both companies now let paying subscribers connect their bank accounts to an AI chatbot through the same third-party data pipe.

The difference is positioning. Perplexity is building outward from institutional finance, with licensed data feeds and audit trails designed for professional research workflows. OpenAI is building inward from consumer convenience, starting with the 200 million people who already ask ChatGPT about their money and giving them a reason to share their actual financial data. The approaches will likely converge, but for now, they reveal different theories about where the value in AI-powered finance actually sits.

The timing is also notable because OpenAI recently introduced advertising into ChatGPT, shifting from a cost-per-thousand-impressions model to cost-per-click within ten weeks of the ads launching. OpenAI says it does not build audience segments from user conversations and does not show ads to users it identifies as under 18. But the structural reality is that the same platform now hosts ads, financial data, and 200 million monthly finance conversations. OpenAI’s privacy controls may be robust, but the combination of advertising and intimate financial data inside a single product will draw scrutiny from regulators, privacy advocates, and users who are accustomed to treating their ChatGPT conversations as private.

The fiduciary question is the one that matters most and receives the least attention. A human financial adviser has a legal obligation to act in a client’s best interest. ChatGPT does not. OpenAI includes a disclaimer that the tool “is not a replacement for professional financial advice,” but that caveat sits alongside a product experience designed to feel like professional financial advice. The gap between what the product looks like and what it legally is, is where the risk lives.

Javelin Research analyst Dylan Lerner described OpenAI’s back-to-back fintech acquisitions as an aggressive push into financial services, positioning the company to own what he called “share of mind” in consumer finance. PitchBook fintech analyst Rudy Yang called personal finance one of the most talked-about use cases for generative AI. The consensus is that OpenAI is not entering banking. It is building something that sits above banking: a conversational layer through which consumers interact with their money, potentially disintermediating the banks and fintechs whose accounts it aggregates.

The feature is currently limited to Pro subscribers, the $200-per-month tier that gives access to OpenAI’s most capable models. OpenAI says it will expand to Plus subscribers after learning from early usage. The company’s broader commercial strategy, which now spans consumer subscriptions, enterprise deployment vehicles, developer APIs, and advertising, increasingly resembles a platform play in which financial data is another input to a system designed to know everything about its users.

Plaid’s chief technology officer, Will Robinson, framed the partnership as a signal of where consumer financial experiences are headed. Plaid’s research suggests 64% of consumers who have used AI for finances say it improved their ability to evaluate financial products, and 53% say it helped them manage day-to-day spending. The numbers are encouraging for adoption. Whether they should be encouraging for the people whose data is flowing through the system is a different question.

For now, OpenAI is betting that the answer to “should I connect my bank account to a chatbot that also shows me ads?” is yes, provided the chatbot is useful enough. Two hundred million monthly finance conversations suggest the demand is there. The question is whether the trust is.

{kind=link}